“Bangalore to host country’s first global Bitcoin conference in December” read the headlines on ET. For a concept non-existent five years ago to grow to a 50,000 strong community owning over 11mn bitcoins worth more than $9bn, it has certainly gone a long way.

What exactly is a bitcoin?

Simply put, it is a form of digital currency that is not regulated by any central authority. The currency exists in a peer-to-peer form of network. For those who are familiar with torrents, the P2P network used in bitcoins is somewhat similar. Here is the wiki link.

How does it work?

In layman terms, a bitcoin is just a bunch of numbers plugged into a mathematical formula representing a unit of currency. Bitcoins are stored in a wallet which stores a unique address(es) for every user. A user may have multiple addresses with multiple amounts of bitcoins stored in them just like how you would hold cash in your wallet. The difference is that since bitcoins are in some sort of encrypted form, you will never be able to find out how much bitcoins I have in my wallet if I give you my address, unlike a real wallet where you can simply count the cash.

Technically speaking, the ‘mathematical formulas’ are essentially cryptographic hash functions. These kinds of functions are typically used in digital signatures, encryption of payment information when you do an online transaction, encryption of email messages that you send to friends so that nobody else is able to intercept the message and so on.

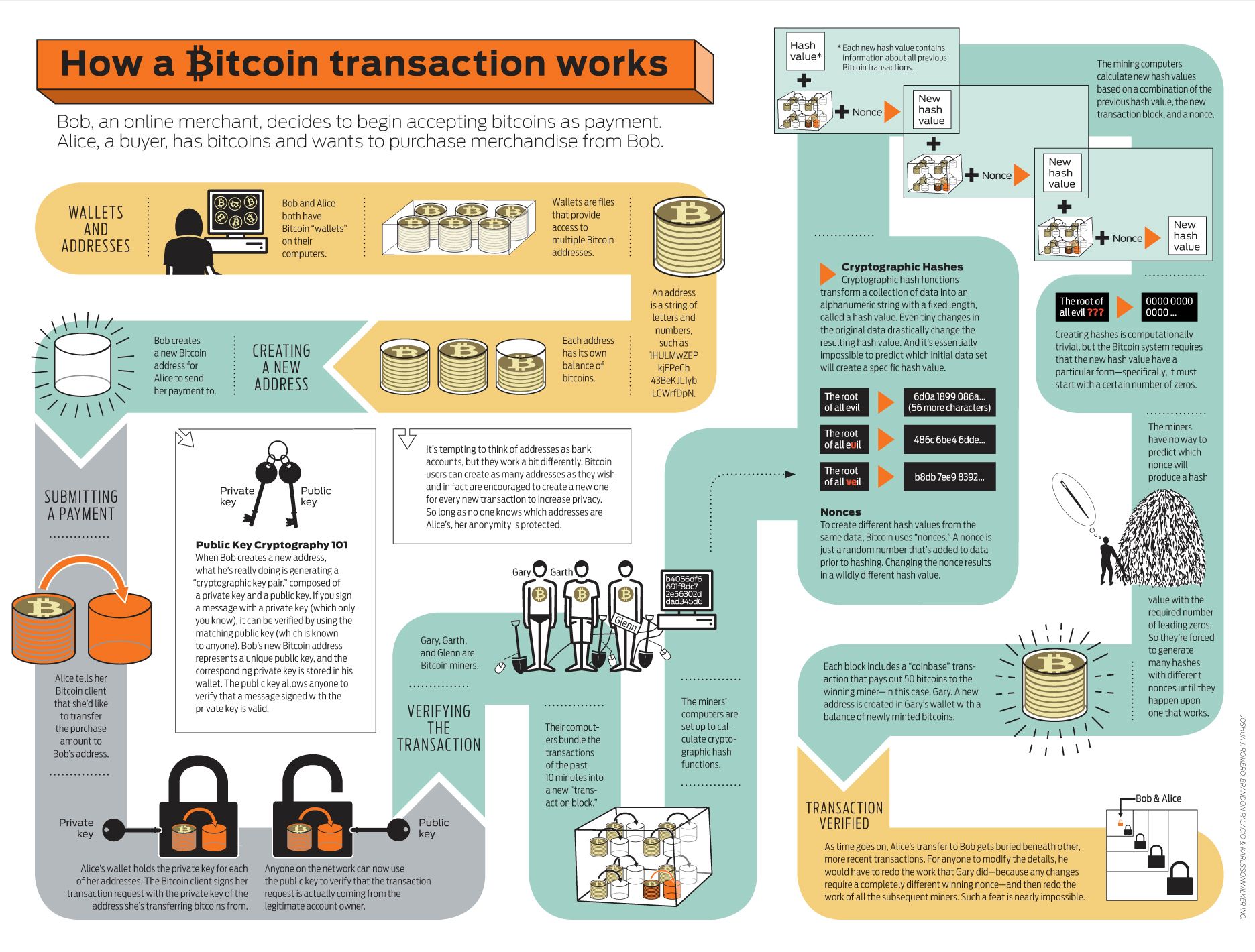

How does a bitcoin transaction happen?

The image below captures this beautifully.

Let’s say you make a transaction using your address and a certain amount of bitcoins. The details of the transaction are encoded using the specified algorithm (cryptography hash functions) and is added to all the other previous transactions ever made in bitcoins. The data is stored in the form of ‘blocks’ with each block having a certain number of transactions. Different blocks are connected to each other to form a ‘blockchain’. Essentially a blockchain will contain crypto hash information about every single transaction ever made in the world in bitcoins.

Even without any understanding of how cryptographic hash functions work, one can see that increasing number of transactions will require an increasingly proportionate amount of disk space as well as computing power to process such large volumes. Here is where the bitcoin ‘miners’ enter. They are people who have access to high performance computers and are willing to give in the time and effort for creating these hash values and they get paid commissions. This is how one earns bitcoins.

Who can create bitcoins?

Anyone. Remember, it is a P2P network. You just need a good processing power in your computer to start ‘mining’ bitcoins. Actually ‘good’ is an understatement here. In addition to the large volume of data to be hashed, the algorithm itself is so complex that it takes a lot more than just buying a fast processor. Huge investments have been made on larger CPUs, drives and other periphery by the miners. For a perspective, check out these sites:

https://en.bitcoin.it/wiki/Mining_hardware_comparison

http://gizmodo.com/5994446/digital-drills-the-monster-machines-that-mine-bitcoin

There are also some ways to get bitcoins for free. Some such sites are:

http://bitcointree.net/links

http://freebitcoinsites.info/

http://btcgeek.com/free-bitcoin/

The only catch is that these sites give you free coins at the rate of a few µbitcoin (micro bitcoin or one millionth of a bitcoin!) which makes it practically useless.

Who started this?

They say it is a chap who goes by the name ‘Satoshi Nakamoto’. Nobody knows who he/she is and this person apparently disappeared from the bitcoin world in 2010. Some folks have created an urban legend that his name is a portmanteau of ‘Samsung’, ‘Toshiba’, ‘Nakamichi’ and ‘Motorola’. Some say it is not one person but a group of people who have a patent related to digital currencies whereas others think it is the National Security Agency. I also found this somewhere – In Japanese Satoshi translates into “clear-thinking; quick-witted; wise.” “Naka” can mean “inside” or “relationship” while “moto” is defined as “the origin; the cause; the foundation; the basis.” So we have “clear-thinking” “inside” “the foundation.”

What’s even more interesting is that tech journalists have been trying for years to find out this mystery man. There have been instances were specific people have been stalked and ‘accused’ of being Nakamoto!

Whoever they are, I’m surprised that they didn’t even come forward to claim fame for revolutionizing the crypto world.

What motivated the need for bitcoins?

Some of the arguments given in favour of this currency are as follows.

- Privacy: Bitcoins allow you to make anonymous transactions without having to reveal your identity, unlike credit cards. It’s almost like cash, only digital.

- De-regulation: Since the government can’t ‘print’ bitcoins willy-nilly, they are not subject to inflationary pressure.

- Safety: If a bank goes bust, deposit holders are at risk. Such an event can’t occur with bitcoins.

- Security: Since bitcoins are stored in cryptographic hashed format, it is next to impossible to ‘steal’ someone else’s currency without knowing their ‘private key’. A wallet address represents the ‘public key’ which is used for making transactions whereas a private key is only known/knowable to the owner of the wallet.

Who accepts bitcoins and why?

Who accepts bitcoins and why?

During the initial days of bitcoins, most of its usage was on sites like Silkroad, an online marketplace that sells drugs and other illegal stuff. Though the US FBI seized the website and its assets a few months back, the site continues to operate in a different version accessible only to those who want access to it!

Bitcoins have come a long way since. The Chinese search engine Baidu, Richard Branson’s Virgin Galactic and WordPress are among the big names that have started accepting bitcoins as a mode of payment. Ebay is also seriously considering the option.

Why do they accept it?

It’s all about reaching a critical mass. As more and more people want to use bitcoins as a currency, the merchant sites are forced to accept them.

My take on bitcoins

I do not agree with most of the aforementioned ‘advantages’ of bitcoins.

- It’s not right to say that bitcoins are not subject to inflationary pressure. Inflation is primarily a function of supply and demand. The selling price of a product in a retail store will depend upon its input cost, not just whether the government is able to print bitcoins or not. That input cost will in turn depend upon supply and so on. So Inflation will impact bitcoins as well. The other issue is the exchange rate of bitcoins. Currently it is trading at a rate of 1BTC =945USD. Two days ago this was around 800USD. This makes BTC an inherently risky proposition. Of course if BTC reaches a critical mass then the volatility will also come down proportionately.

- There is great concern that the anonymity of bitcoin transactions will encourage illegal trades – silkroad being a case in point. Personally, I don’t think illegal trades need a digital currency to thrive; if those guys want to do such trades they will surely find a way out – bitcoins or not. But the bigger issue here is that transactions made through bitcoins cannot be reversed under any circumstance. With a credit card transaction, if something goes wrong, you can file a legal case against the issuer as the entire transaction details are available for verification. Even with cash, if you pay at a local grocery store you can go back and ask for a refund. However, with bitcoins since the person you are transacting with is unknown to you, you have absolutely no way of getting back your money if the transaction doesn’t happen as per the terms. There is also no guarantee that the other person will honor their part of the deal as there is no way to prove that such a transaction was entered into in the first place.

- Safety: The safety aspect is a bit different here than a bank going bust. Instead, your computer can crash, taking away your wallet addresses and the precious money along with it. In order to prepare for such contingencies you need to have a backup record of your ‘private key’ somewhere else, which itself is a cumbersome process involving downloading complicated software etc.

- I don’t buy the security argument of bitcoins at all. For one thing, cryptography is not a 100% foolproof mechanism. Time and again it has been seen that old crypto techniques get obsolete as they get hacked into by smarter and smarter cyber criminals. Newer and more complicated crypto algorithms come into play then. The second thing is that this whole database of blockchains and transactions is maintained by a certain group of people – the miners. Your wallet address is known to every one of these miners. Who is to say these miners will always act in your interest and not tamper with the transactions you make?

- Finally, I think that bitcoin is just a fad that will go into oblivion sooner or later as the giant government machineries work towards shutting them down or try to take control over it. There have also been arguments against this possibility. Supporters of bitcoins say that just like how regulators have never been able to completely shut down P2P networks such as bittorrents, they will not be able to do it with bitcoins either. I disagree. In this case all they need to do is to enforce legal sanctions on mainstream corporate that accept bitcoins as a mode of payment. Bitcoin will then simply become the stuff of folklore.

Final words

I have created my own bitcoin wallet from www.coinbase.com . Anyone who wishes to donate some money my way for all the effort I’ve put into this blog may do so at:

1MrZJFro4H9YfoT3X72FohH7vKMiLmdyjt

{kind=link}